Elizabeth Warren Highlights Washington's Losing Housing Battle

by: Larry Doyle

October 11, 2009

Who in Washington will give you a straight answer? Elizabeth Warren.

Who is Elizabeth Warren?

Her Wikipedia bio reads:

Elizabeth Warren (born 1949) is the Leo Gottlieb Professor of Law at Harvard Law School, where she teaches contract law, bankruptcy, and commercial law. In the wake of the 2008-9 financial crisis, she has also become the chair of the Congressional Oversight Panel created to oversee the U.S. banking bailout, formally known as the Troubled Assets Relief Program. In 2007, she first developed the idea to create a new Consumer Financial Protection Agency, which President Barack Obama, Christopher Dodd, and Barney Frank are now advocating as part of their financial regulatory reform proposals.

In May 2009, Warren was named one of Time Magazine’s 100 Most InfluentialPeople in the World.

Ms. Warren consistently takes no prisoners or provides no pandering in making honest assessments of the interaction between Washington and Wall Street. She has called the banks on the carpet. She has called Secretary Geithner on the carpet. She has called Congress on the carpet. Why? A general lack of honesty, integrity, and transparency in dealing with the American public.

When she speaks, I listen.

What did she have to say Friday morning? In commenting on a recently released report on the effectiveness of government programs to support housing, Warren questioned the scalability and the permanence of the impact of the TARP funding. Bloomberg provides further color in writing Friday morning TARP Oversight Group Says Treasury Mortgage Plan Not Effective.

The report highlights,

“Rising unemployment, generally flat or even falling home prices and impending mortgage-rate resets threaten to cast millions more out of their homes,” the report said. “The panel urges Treasury to reconsider the scope, scalability and permanence of the programs designed to minimize the economic impact of foreclosures and consider whether new programs or program enhancements could be adopted.”

New programs or program enhancements? On Thursday I opined in Washington Needs a New Housing Model:

While the administration swims upstream on this issue, bank policy of tight credit and restrictive lending only further exacerbates the housing market. Make no mistake, though, banks are taking that approach to tight credit at the behest of regulators who know the level of losses in the banking system and are trying to preserve the industry as a whole.

I like a rallying equity market as much as anybody, but I wouldn’t spend any paper gains just yet. Why? The new housing model is displaying that:

“As defaults become more common, the social stigma attached with defaulting will likely be reduced, especially if there continues to be few repercussions for people who walk away from their loans,” concluded Sapienza. “This has an adverse effect on homeowners who do pay their mortgages, and the after-effects of more defaults and more price collapse could be economic catastrophe.”

This model needs some quick-dry crazy glue, which could only be applied in the form of a serious principal reduction program. Banks would take immediate and massive hits to capital which they clearly won’t accept.

So how can we generate some support for housing?

Aside from a principal reduction program, the penalty for those who would strategically default on their mortgage needs to be far more onerous.

The principal reduction would negatively impact bank earnings. Too bad. The banks are feeding at the taxpayer trough currently and would not be here without the bailouts. The individuals who are capable of making their payments need to accept the moral responsibility that is embedded in a contract.

Although given the massive violation of moral hazards and breaking of contracts by Uncle Sam, that old man does not have a lot of credibility on that front.

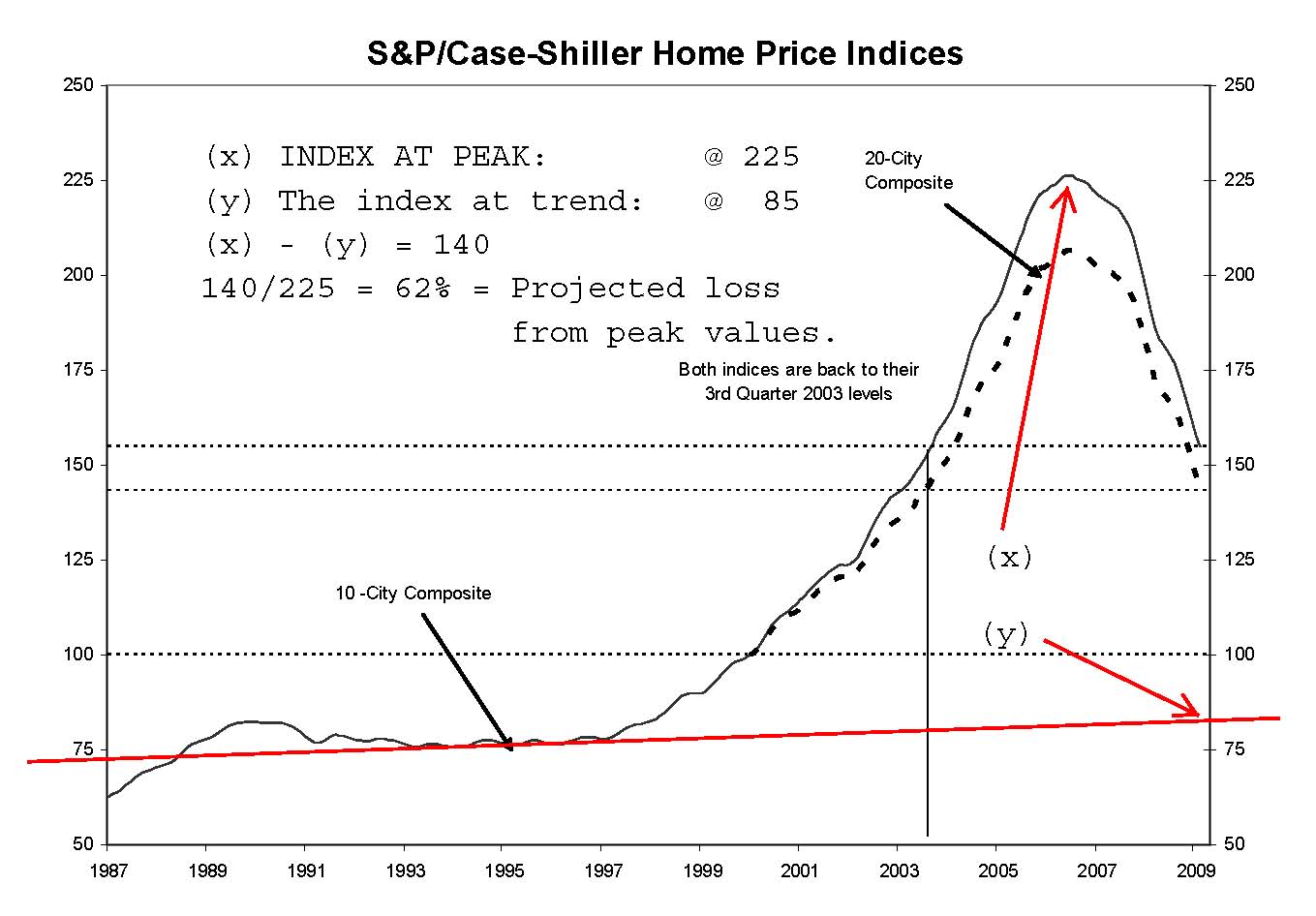

What do we really learn here? Ultimately the market is the market and efforts to manipulate or support a falling market will only be temporary. The market needs to find the clearing level where private money will purchase properties. That private money will wait while Uncle Sam continues to try to prop the market.

In the meantime, do not expect any meaningful support for housing.