Let's ponder the national scene for a moment and you can draw your own conclusions as to where Hoboken price expectations need to drop in RE.ality.

Single family homes are the bedrock of high-end sales in Hoboken (no, not the cookie cutter trash being sold to you at the W or Maxwell Place). They have a good history of comparables and the structures are mostly original, except for some rehab adjustments.

Nationally, September 2009 single family home sales broke down like this:

21% = less than $100k

49% = $100K to $250k

22% = $250 to $500K

5.6% = $500k to $750K

1.3% = $750k to $1mio

1.3% = $1mio and up

These are national numbers. Is it any wonder that a city such as Hoboken, with a heavy dependence on the NYC growth has stopped dead in its tracks? Ah yes, there's month to month improvement for the last several months. Granted. But when you're looking down a big black hole, is this bounce even something to cheer about?

Only 8.2% of all such sales nationwide were for $500K or more. Less than 10%!

Or another way, 70% of all such sales were for under $250K! How much single family inventory in Hoboken is priced at that level? I'm going to guess... none!

So where will those buyers eventually come from?

Well, year to year doesn't help the rose-colored view either.

<$100k +22.5%

$100K-$250K +6%

$250K-$500K -5.2%

$500k-$750K +4.0%

$750K-$1mio -2.6%

$1mio up -1.2%

While there's plenty to cheer about from the beginning of the year, it would seem that the disaster is just underway for the prospects of this mighty NYC wanna be; at least as far as RE.ality is concerned.

The next time your broker tells you that affordability has never been better, I suggest you think about where affordability needs to be.

Tuesday, October 27, 2009

Monday, October 26, 2009

NY Times: Fair Game

If Lenders Say ‘The Dog Ate Your Mortgage’

FOR decades, when troubled homeowners and banks battled over delinquent mortgages, it wasn’t a contest. Homes went into foreclosure, and lenders took control of the property.

On top of that, courts rubber-stamped the array of foreclosure charges that lenders heaped onto borrowers and took banks at their word when the lenders said they owned the mortgage notes underlying troubled properties.

In other words, with lenders in the driver’s seat, borrowers were run over, more often than not. Of course, errant borrowers hardly deserve sympathy from bankers or anyone else, and banks are well within their rights to try to protect their financial interests.

But if our current financial crisis has taught us anything, it is that many borrowers entered into mortgage agreements without a clear understanding of the debt they were incurring. And banks often lacked a clear understanding of whether all those borrowers could really repay their loans.

Even so, banks and borrowers still do battle over foreclosures on an unlevel playing field that exists in far too many courtrooms. But some judges are starting to scrutinize the rules-don’t-matter methods used by lenders and their lawyers in the recent foreclosure wave. On occasion, lenders are even getting slapped around a bit.

One surprising smackdown occurred on Oct. 9 in federal bankruptcy court in the Southern District of New York. Ruling that a lender, PHH Mortgage, hadn’t proved its claim to a delinquent borrower’s home in White Plains, Judge Robert D. Drain wiped out a $461,263 mortgage debt on the property. That’s right: the mortgage debt disappeared, via a court order.

So the ruling may put a new dynamic in play in the foreclosure mess: If the lender can’t come forward with proof of ownership, and judges don’t look kindly on that, then borrowers may have a stronger hand to play in court and, apparently, may even be able to stay in their homes mortgage-free.

The reason that notes have gone missing is the huge mass of mortgage securitizations that occurred during the housing boom. Securitizations allowed for large pools of bank loans to be bundled and sold to legions of investors, but some of the nuts and bolts of the mortgage game — notes, for example — were never adequately tracked or recorded during the boom. In some cases, that means nobody truly knows who owns what.

To be sure, many legal hurdles mean that the initial outcome of the White Plains case may not be repeated elsewhere. Nevertheless, the ruling — by a federal judge, no less — is bound to bring a smile to anyone who has been subjected to rough treatment by a lender. Methinks a few of those people still exist.

More important, the case is an alert to lenders that dubious proof-of-ownership tactics may no longer be accepted practice. They may even be viewed as a fraud on the court.

The United States Trustee, a division of the Justice Department charged with monitoring the nation’s bankruptcy courts, has also taken an interest in the White Plains case. Its representative has attended hearings in the matter, and it has registered with the court as an interested party.

THE case involves a borrower, who declined to be named, living in a home with her daughter and son-in-law. According to court documents, the borrower bought the house in 2001 with a mortgage from Wells Fargo; four and a half years later she refinanced with Mortgage World Bankers Inc.

She fell behind in her payments, and David B. Shaev, a consumer bankruptcy lawyer in Manhattan, filed a Chapter 13 bankruptcy plan on her behalf in late February in an effort to save her home from foreclosure.

A proof of claim to the debt was filed in March by PHH, a company based in Mount Laurel, N.J. The $461,263 that PHH said was owed included $33,545 in arrears.

Mr. Shaev said that when he filed the case, he had simply hoped to persuade PHH to modify his client’s loan. But after months of what he described as foot-dragging by PHH and its lawyers, he asked for proof of PHH’s standing in the case.

“If you want to take someone’s house away, you’d better make sure you have the right to do it,” Mr. Shaev said in an interview last week.

In answer, Mr. Shaev received a letter stating that PHH was the servicer of the loan but that the holder of the note was U.S. Bank, as trustee of a securitization pool. But U.S. Bank was not a party to the action.

Mr. Shaev then asked for proof that U.S. Bank was indeed the holder of the note. All that was provided, however, was an affidavit from Tracy Johnson, a vice president at PHH Mortgage, saying that PHH was the servicer and U.S. Bank the holder.

Among the filings supplied to support Ms. Johnson’s assertion was a copy of the assignment of the mortgage. But this, too, was signed by Ms. Johnson, only this time she was identified as an assistant vice president of MERS, the Mortgage Electronic Registration System. This bank-owned registry eliminates the need to record changes in property ownership in local land records.

Another problem was that the document showed the note was assigned on March 26, 2009, well after the bankruptcy had been filed.

Mr. Shaev’s questions about ownership also led to an admission by PHH that, along the way, it had levied an improper $450 foreclosure fee on the borrower and had overcharged interest by an unstated amount.

John DiCaro, a lawyer representing PHH at the hearing, was in the uncomfortable position of having to explain why there was no documentation of an assignment to U.S. Bank. He did not return a phone call seeking comment last week. Ms. Johnson, who couldn’t be reached for comment, did not attend the hearing.

According to a transcript of the Sept. 29 hearing, Mr. DiCaro said: “In the secondary market, there are many cases where assignment of mortgages, assignment of notes, don’t happen at the time they should. It was standard operating procedure for many years.”

Judge Drain rejected that argument, concluding that what had been presented to the court just did not add up. “I think that I have a more than 50 percent doubt that if the debtor paid this claim, it would be paying the wrong person,” he said. “That’s the problem. And that’s because the claimant has not shown an assignment of a mortgage.”

Mr. Shaev said he was shocked when the judge expunged the mortgage debt.

“We are in uncharted territory,” he said. “Right now I am in bankruptcy court with a house that has no discernible debt on it, yet I have a client with a signed mortgage. We cannot in theory just go out and sell this house because the title company won’t give a clear title on it.”

Among the next steps Mr. Shaev said he would take is to file an amended plan or sue to try to get clear title to the property.

Late last week, PHH appealed the judge’s ruling. But Mr. DiCaro and PHH are in something of a bind. Either they will return to court with a clear claim on the property — including all the transfers and sales that are necessary in the securitization process — or they won’t be able to produce that documentation. If they do produce it, they will then have to explain why they didn’t produce it before.

Oh, what a tangled web these mortgage lenders weave.Tuesday, October 20, 2009

Monthly RE.ality Check from Michael David White

The following is a national perspective with the foundation that Hoboken's factors are going to underperform for the foreseeable future.

----------------------------------------------------------

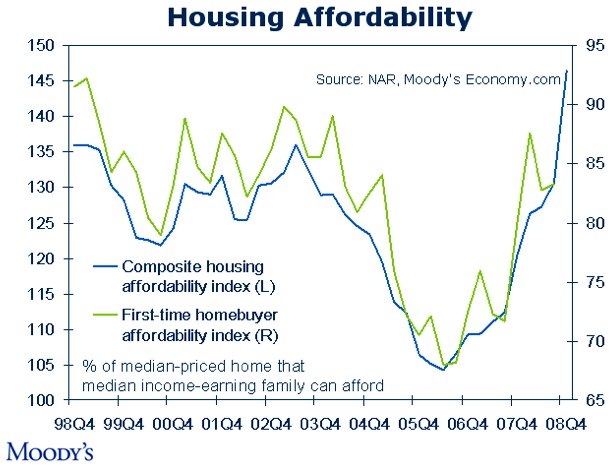

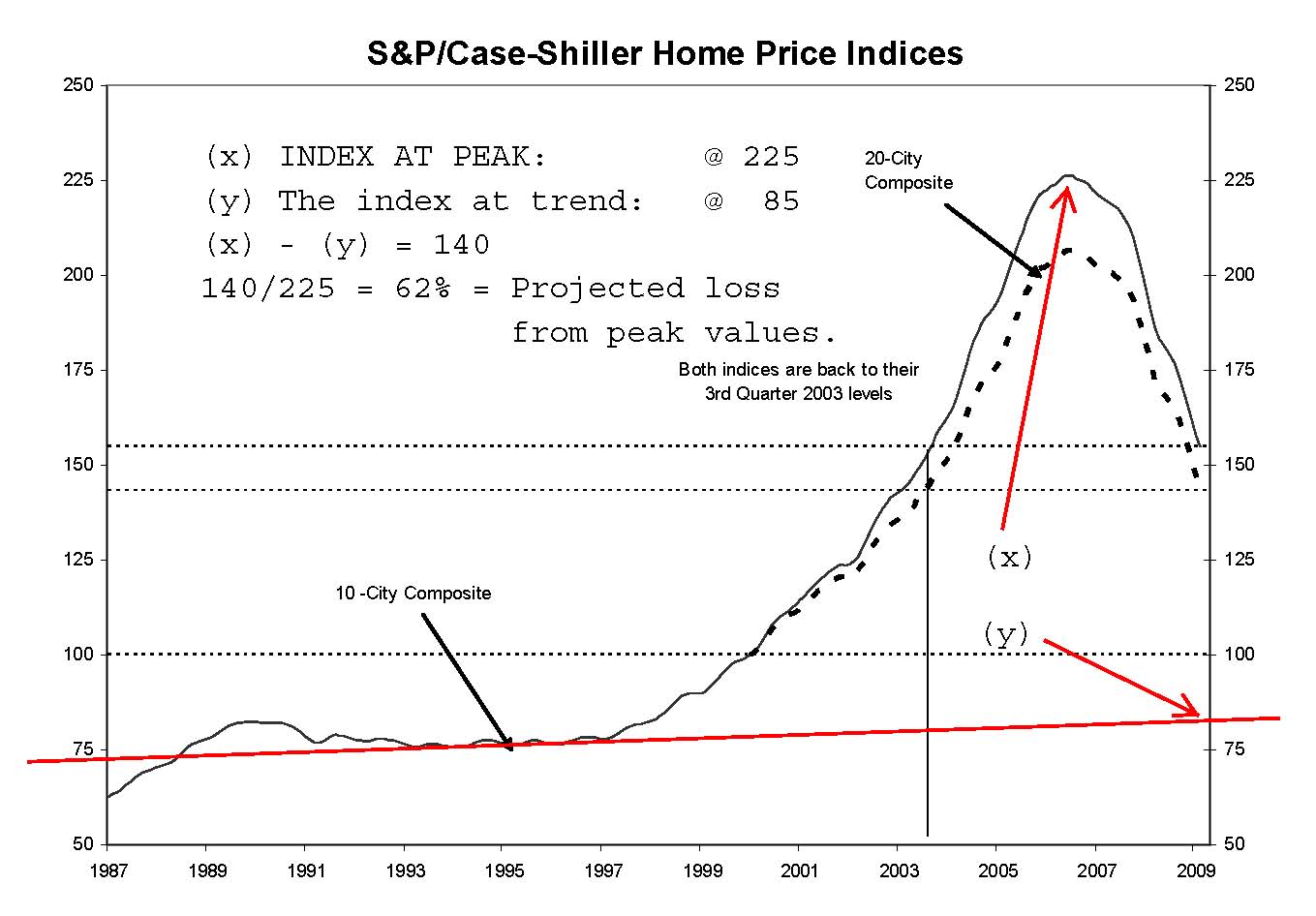

The good news is that recent price trends are strong in residential real estate. We have a quarter of price growth in the bag. Prices have also fallen so far since the summer-of-2006 peak that affordability is roughly equal to what it was at the turn of the century (2000). Nobody can argue that a fall of 30% doesn’t make it easier to buy. Is it the best time to buy?

----------------------------------------------------------

The good news is that recent price trends are strong in residential real estate. We have a quarter of price growth in the bag. Prices have also fallen so far since the summer-of-2006 peak that affordability is roughly equal to what it was at the turn of the century (2000). Nobody can argue that a fall of 30% doesn’t make it easier to buy. Is it the best time to buy?

click to enlarge

The bad news is that the financial media is incapable of balancing competing and complicating factors which any buyer of real estate must review.

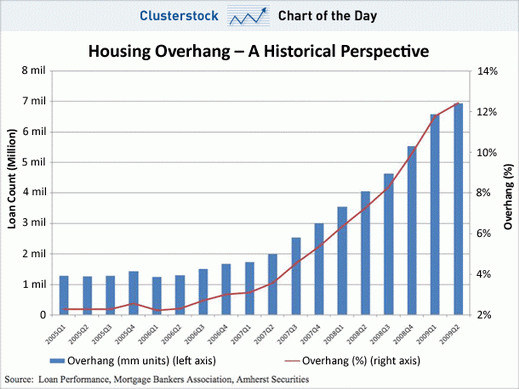

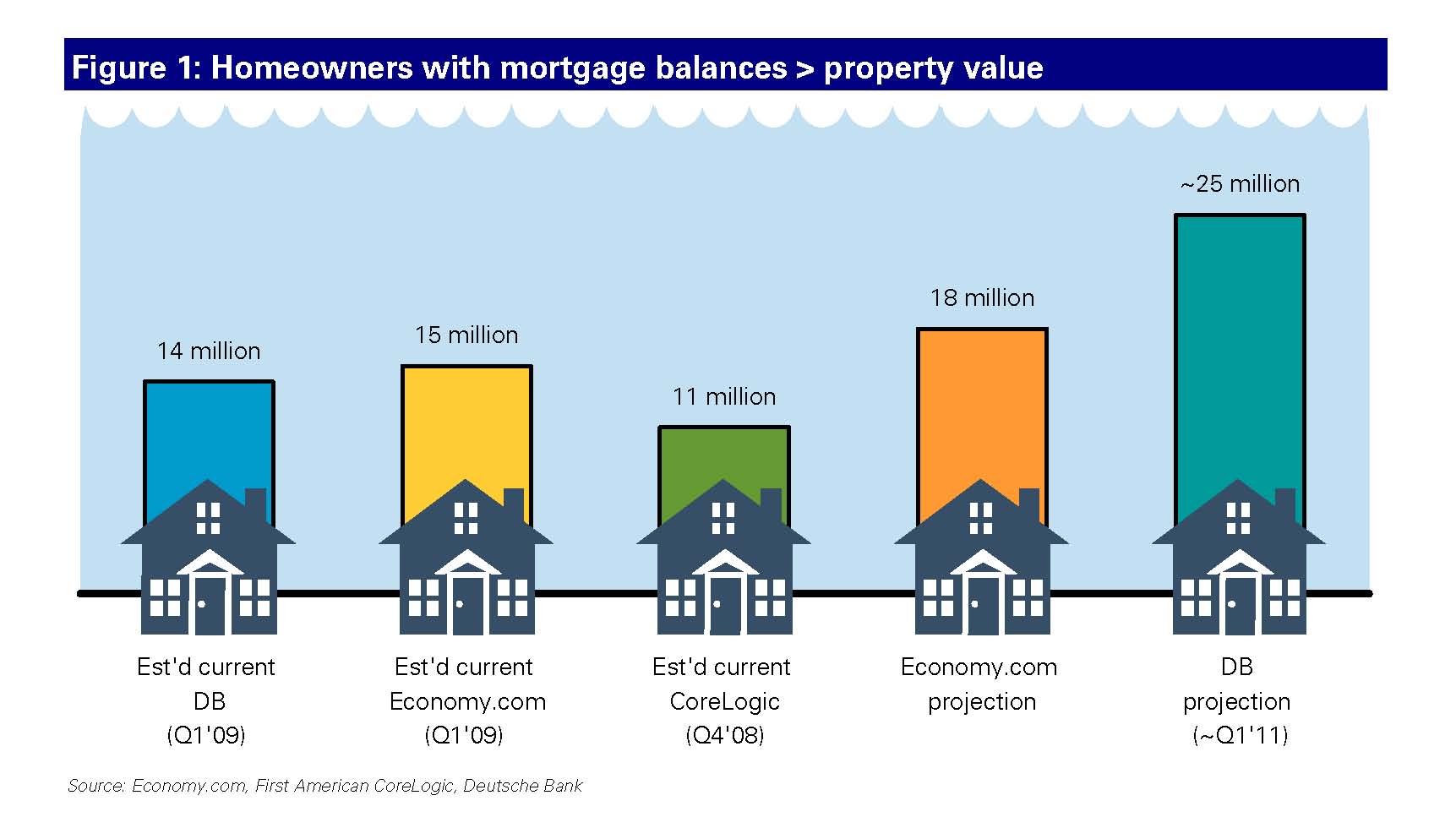

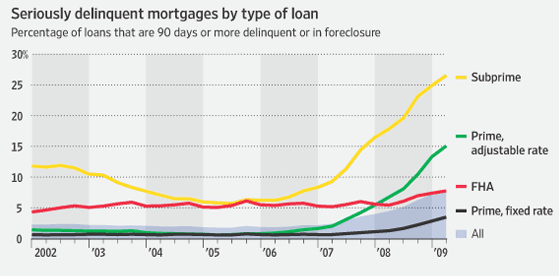

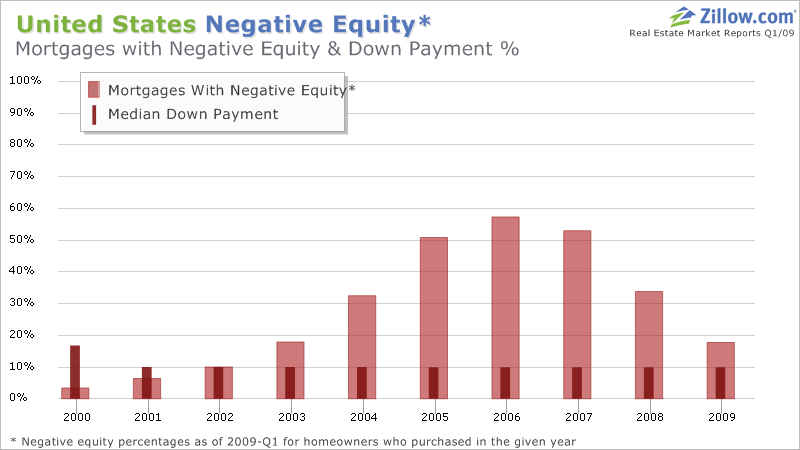

If you look at mortgage payments and the number of past due accounts; if you look at the number of properties which are approaching or are now in negative equity (in which mortgage debt exceeds the value of the house); if you look at the supply of existing (not new) properties for sale; if you look at the systemic debt levels of consumers and of American society as a whole; if you look at unemployment; and if you look at the trends which history dictates after a credit crisis; if you look at all of these major factors, they are all negative for real estate.

Balancing these factors requires the intelligence to incorporate many different variables; a balance which is impossible on a breaking news story. All of these variables create a fuller opinion on the future of property values. You need this information to make a good decision about your most important investment – the purchase of your home. Look at the charts. Glance at the captions. What feeling does it leave you with? That feeling should be your “buy” or “sell” indicator.

The daily media is simply a dumb conformist blind man--chasing the latest number with no regard to competing claims, no memory, and no common sense.

You can’t be fooled again on the value of real estate.(Page Down or Click here to see "Property Values: Ten Key Charts & Critical Commentary" -- a 360-degree view of property values.)

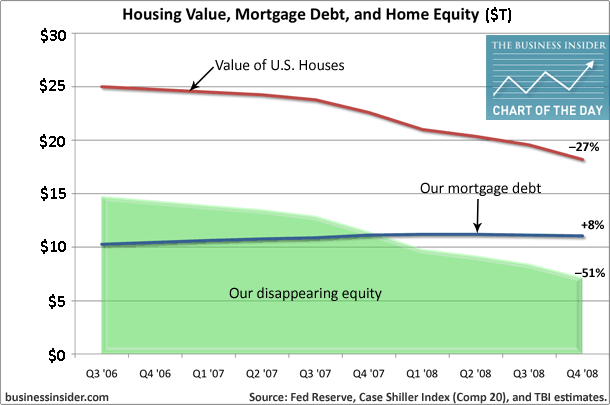

EQUITY VANISHES: About $7 trillion has been taken from the wealth account of property owners. If there are 130 million housing units in the United States (rental and owner occupied), then owners have lost an average of $54,000 per unit they own. The loss is massive.

Green Vomit (9/25): How could anybody say this is a reasonable time to invest in real estate? You could either prove these numbers wrong, or you could check into the mental ward. Have you had your medication today?

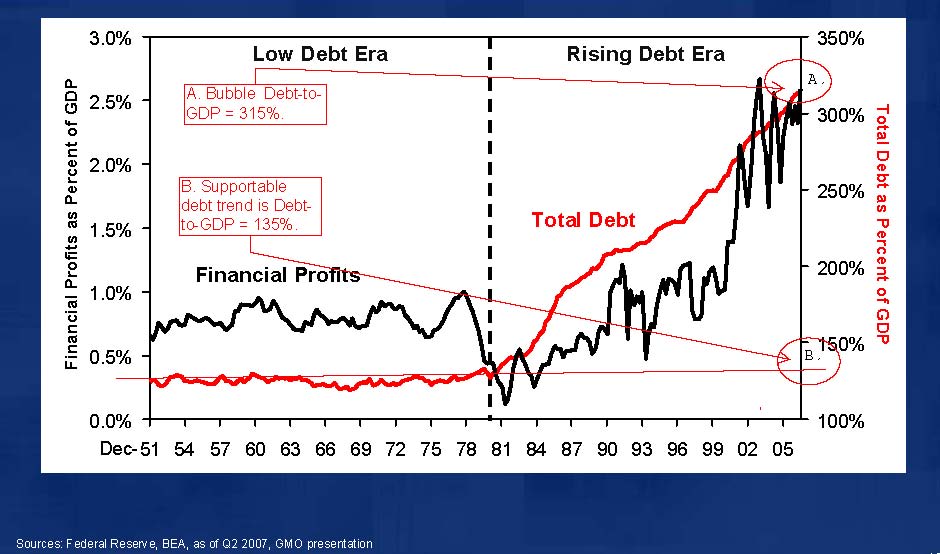

DEBT BE NOT PROUD (8/11/09): One school of thought says excess debt must be paid off or written off before we will achieve dynamic growth. This "Low Debt" and "High Debt" chart of approximately the last 60 years shows that the magnitude of debt, whether it be corporate or household, could be far beyond reasonable. If this school is correct, then we may have many years or even a decade of slow growth. The only cure would be radical steps to reduce debt. If we are in the hang over of a world-record credit bubble, then the outlook for real estate investment is negative.

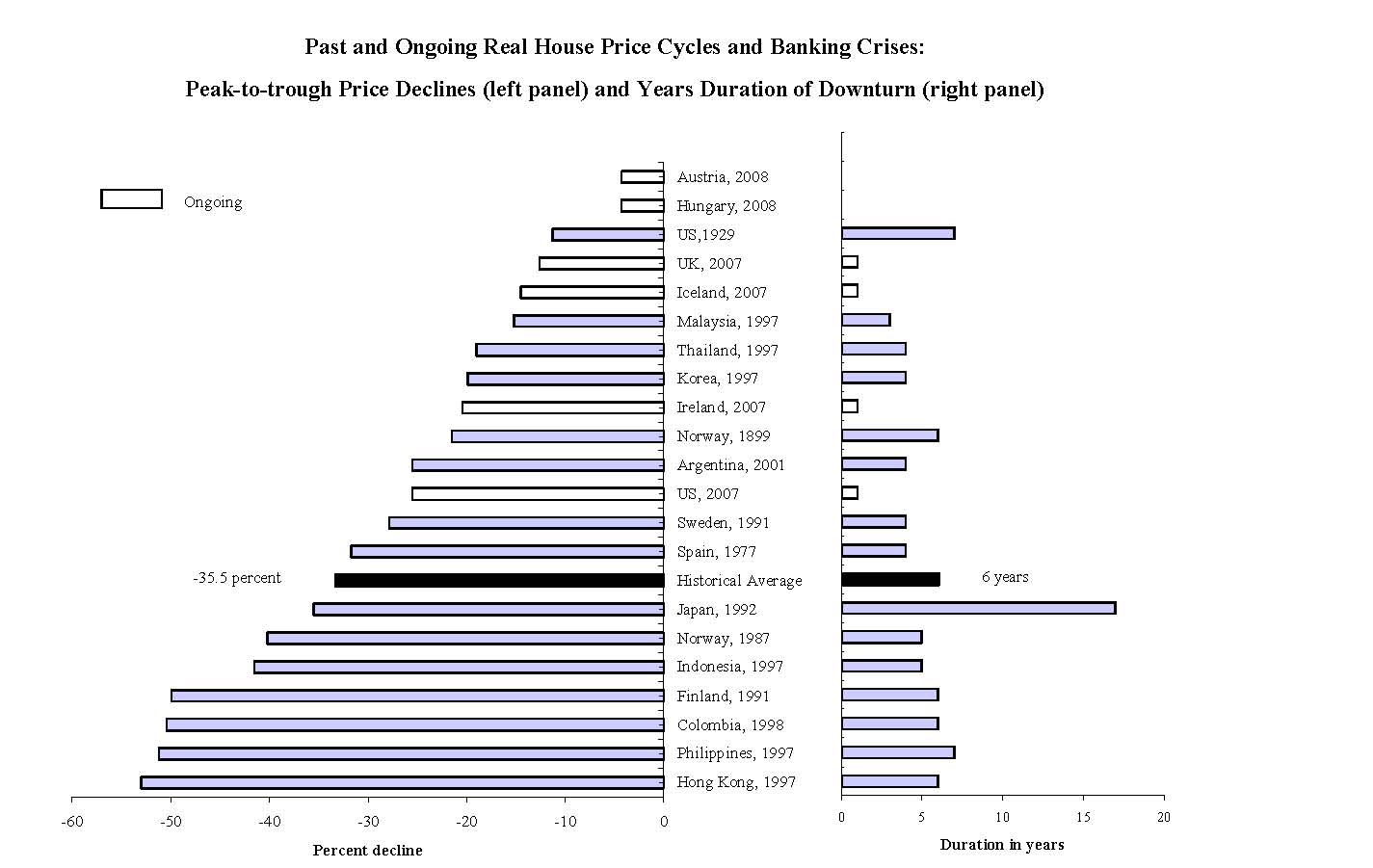

HISTORY'S TRENDS (8/5/09): The best research into credit bubbles says that property's value will fall through the summer of 2012 -- until three years from now. The good news is that the fall in values has nearly equalled the average fall of 35%. The bad news? What if we have a King-Kong credit bubble and it's actually not stupid to say "It's different this time."?

Tuesday, October 13, 2009

The RE Bear Is Very Determined And Healthy

Despite the onset of cold weather, there seems to be little reason for real estate bears to hibernate! One of the very valid points about the big picture on the situation, is the following: if we are stabilizing with all the liquidity and subsidies being thrown at this sector, why would we hope for any positive performance when these are removed? Those arguments would have to entail real economic growth and a shortage of inventory in combination with real job growth! I don't see any way toward such a combination of events coming into play for years to come.

Hoboken will continue to lag and likely diverge from any recovery elsewhere. This will hold true for the entire metro NYC market as we get hit with higher and higher tax supports for gaping budgets. The money is gone! Where will it come from? You guessed it and it isn't going to stop any time in the foreseeable future.

A dedicated reader of this blog forwarded an insightful editorial that sums up the fluff despite today's "discounts" on residential property. The powerful causes for this bubble are summed up in the final paragraph.

---------------------------------------------

No Exit

Treasury contemplates yet more aid for housing.

Hoboken will continue to lag and likely diverge from any recovery elsewhere. This will hold true for the entire metro NYC market as we get hit with higher and higher tax supports for gaping budgets. The money is gone! Where will it come from? You guessed it and it isn't going to stop any time in the foreseeable future.

A dedicated reader of this blog forwarded an insightful editorial that sums up the fluff despite today's "discounts" on residential property. The powerful causes for this bubble are summed up in the final paragraph.

---------------------------------------------

No Exit

Treasury contemplates yet more aid for housing.

Monday, October 12, 2009

HOW BADLY DID the U.S. housing market crash? Well, just look at how much federal aid it has taken to stabilize it, at least for now. The Federal Reserve has bought almost $700 billion worth of mortgage-backed securities, with more to come. The Treasury Department is covering the losses of Fannie Mae and Freddie Mac. Congress has enacted tax credits to spur home buying, including an $8,000 bonus to first-time buyers that expires Nov. 30 but may well be extended. The Federal Housing Administration has dramatically expanded its mortgage insurance portfolio. The Obama administration offers government-backed refinancing to middle-income homeowners who are up to 25 percent underwater in their current mortgages.

Yet housing remains burdened by a huge backlog of unsold homes, which will probably grow since more foreclosures are on the way. And so the Treasury Department is contemplating yet more help, this time in the form of backstopping state-issued mortgage-revenue bonds, which are federally subsidized in that investors collect the interest tax free. During the boom, the states' housing finance agencies used these bonds to fund about 100,000 low-interest mortgages per year for lower-income home buyers. But since the bust, private bond buyers have shunned them, notwithstanding their tax-free status. At $4 billion this year, mortgage-revenue bond sales are running at a quarter of the pace they set in 2007, according to Thomson Reuters. The plan under discussion would have the government purchase about $20 billion worth of new bonds before the end of the year while insuring $15 billion in existing securities that states otherwise might be forced to redeem because they would not be tradable in the markets.

Administration officials are considering steps to limit the risk to taxpayers by, for example, charging a fee to back those bonds that Treasury does not buy outright. It is also true that, in the past, borrowers of bond-backed mortgages, well selected by the states, have defaulted relatively rarely. Of course, past borrowers didn't face anything like today's unemployment and foreclosure rates. Indeed, those conditions partly explain why private investors have bowed out of the market. As compared to other more direct forms of housing aid, mortgage-revenue bonds also come with high associated costs, in the form of fees for lawyers, rating agencies and underwriters.

Compared to the overall size of the huge housing bailout, this latest policy idea is pretty small beer. It does illustrate, though, that Washington is still in crisis mode when it comes to thinking about a vast, strategic sector of the economy. That's perhaps understandable, but it can't go on indefinitely. The financial crisis was partly the result of years of government-encouraged over-investment in residential real estate. When will the federal government start working on an exit strategy and a new, more rational housing policy -- one in which individual homeownership occupies a central, but less heavily subsidized, position? The answer, apparently, is not yet.

Monday, October 12, 2009

Foreclosures Grow In Housing Market's Top Tiers

Foreclosures Grow In Housing Market's Top Tiers

By NICK TIMIRAOS

Of THE WALL STREET JOURNAL

Of THE WALL STREET JOURNAL

New data suggest that foreclosures are rising in more expensive housing markets.

About 30% of foreclosures in June involved homes in the top third of local housing values, up from 16% when the foreclosure crisis began three years ago, according to new data from real-estate Web site Zillow.com. The bottom one-third of housing markets, by home value, now account for 35% of foreclosures, down from 55% in 2006.

The report shows that foreclosures, after declining earlier this year, began to accelerate in the late spring and that more expensive homes have more recently accounted for a growing share of all foreclosures. "The slope of that curve in recent months is much sharper than it was recently," said Stan Humphries, chief economist for Zillow. Rising foreclosures among more-expensive homes could create added pressure for a housing market that has shown signs of stabilizing in recent months as sales of lower-priced homes pick up.

The Zillow research compared homes against the median values for their local market and broke each market into three tiers by value. Zillow then looked at the share of monthly foreclosures in each tier over the past decade.

(This story and related background material will be available on The Wall Street Journal Web site, WSJ.com.)

Foreclosures are rising in more expensive markets as home values in those areas fall, leaving more homeowners with mortgages that exceed the value of their properties. Prime loans accounted for 58% of foreclosure starts in the second quarter, up from 44% last year, according to the Mortgage Bankers Association. Subprime mortgages accounted for one-third of foreclosure starts, down from one-half last year.

The prime category includes so-called exotic mortgages that were increasingly used to buy more expensive homes, including interest-only mortgages that allowed borrowers to defer principal payments during an initial period. Borrowers often aren't able to refinance out of these products because the drop in home values has left them with little equity in their homes.

Default rates are particularly high and expected to rise on option adjustable-rate mortgages, which allow borrowers to make minimum payments that may not cover the interest due. Monthly payments can increase to sharply higher levels after five years or when the outstanding balance reaches a certain level. A study by Fitch Ratings found that 46% of option ARMs were 30 days past due last month, even though just 12% of such loans have reset to higher monthly payments.

Zillow estimated that nearly one in four homes with mortgages was worth less than the value of the property at the end of June. Mr. Humphries said he didn't expect to see foreclosure volumes level off until later in 2010.

Sunday, October 11, 2009

Rising U.S. Vacancies: Real Estate Is Headed Down

Rising U.S. Vacancies: Real Estate Is Headed Down

by: Jeff Nielson

October 11, 2009

Two pieces of data on U.S. vacancy rates (one commercial, one residential) show in unequivocal terms that house prices are going to continue lower, while the more-recent collapse in commercial real estate will continue to accelerate.

The U.S. vacancy rates for rental apartments has just hit its highest rate in 23 years – and is set to continue moving higher with new construction vastly outpacing sales. This guarantees that rent prices will drop (especially in an environment of rising unemployment and falling wages). It is equally certain that falling rent prices will translate into falling prices for U.S. residential real estate.

Falling rent prices make buying a home relatively more expensive (not to mention the risk of defaulting on a mortgage should the buyer lose his employment). This will continue to put downward pressure on U.S. house prices – adding to the downward pressure caused by rising unemployment, record-rates of foreclosures, more than 20 million empty homes (including millions of foreclosed properties being held off the market), and the need for retiring baby-boomers to sell real estate to fund their retirements (see “U.S. pension crisis: the $3 TRILLION question”).

The momentary stabilization in U.S. housing prices is nothing more than a combination of months of relentless propaganda proclaiming a “bottom” in this market – along with the minor boost to the economy from the Obama stimulus package, and the normal “seasonal strength” of this market in the summer.

Almost certainly these prices will resume their downward march in the next few weeks. The only thing which could alter this picture is if U.S. inflation (which the government pretends doesn't exist) should accelerate so rapidly that “up” becomes “down”. In other words, if U.S. inflation (currently around 7% in the real world) should heat-up to double-digits, we could see small nominal gains in U.S. prices – which in real dollars would still be steadily depreciating.

Meanwhile, in the commercial sector, the vacancy rate just hit its highest level in 5 years (reflecting the fact that this market hasn't been collapsing for as long as the housing market). It is a certainty that this rate will continue soaring higher – given that both corporate revenues and corporate earnings are still plunging downward at double-digit rates (see “Crash warnings abound for U.S. markets”).

This means that U.S. banks can expect sky-rocketing losses on their commercial mortgage portfolio (in this $6 trillion market). As I have pointed out in previous commentaries, U.S. banks have virtually nothing set aside for these losses. This was echoed by a presentation from the Federal Reserve to banking regulators last month – and is an “instant replay” of what happened with U.S. banks when the housing market crashed.

The main difference between this new source of mounting losses on this category of bank loans is that unlike with the crash in residential real estate, this crash comes at the same time that all other categories of U.S. debt are already at or near record-levels of delinquencies (i.e. loans where the banks are not getting paid). The combination of huge losses these banks must absorb on commercial defaults while they are not receiving payments from record numbers of borrowers in all other categories of debt, and having virtually no reserves to cover these losses creates a very painful dilemma for the banksters.

As I have stated unequivocally on numerous occasions (and which George Soros just echoed in a recent interview), U.S. big-banks remain insolvent. With new, rising losses and tiny capital cushions, it appears that some or all of them will be forced to get in line for their next series of government blank-cheques. The problem is how can the Wall Street crime syndicate beg for more hand-outs from the government while these fraud-factories claim to be making “profits”?

Once again, the perfect “recipe” for Wall Street appears to be to induce a broad, general panic – which could frighten both the spineless politicians and the American public enough for them to capitulate to more bankster blackmail. Given that most recent, U.S. economic data has still been terrible (despite what media spin-doctors would like us to believe), it would take nothing more than telling the truth to “pop” the U.S. equities bubble – and begin another fear cycle.

As a reminder, John Williams' “Shadowstats.com” (the most widely-accepted source for real numbers on the U.S. economy) has calculated current U.S. unemployment at over 20% (and still rising rapidly). Meanwhile, the fantasy-world presented by the propaganda-machine continues to pretend that things are getting better for the unemployed, and soon-to-be-unemployed.

This disconnect cannot continue. The absolute end-point for the fantasy-rally in U.S. equity markets is early December – the time at which it will be clear that this year's holiday shopping season will be a big disappointment for this consumer economy. However, there are an endless number of possible triggers between now and then (including the banksters proclaiming they need more hand-outs). For those who have continued to ignore six solid months of rising insider-selling, it's time to take your money and run.

by: Jeff Nielson

October 11, 2009

Two pieces of data on U.S. vacancy rates (one commercial, one residential) show in unequivocal terms that house prices are going to continue lower, while the more-recent collapse in commercial real estate will continue to accelerate.

The U.S. vacancy rates for rental apartments has just hit its highest rate in 23 years – and is set to continue moving higher with new construction vastly outpacing sales. This guarantees that rent prices will drop (especially in an environment of rising unemployment and falling wages). It is equally certain that falling rent prices will translate into falling prices for U.S. residential real estate.

Falling rent prices make buying a home relatively more expensive (not to mention the risk of defaulting on a mortgage should the buyer lose his employment). This will continue to put downward pressure on U.S. house prices – adding to the downward pressure caused by rising unemployment, record-rates of foreclosures, more than 20 million empty homes (including millions of foreclosed properties being held off the market), and the need for retiring baby-boomers to sell real estate to fund their retirements (see “U.S. pension crisis: the $3 TRILLION question”).

The momentary stabilization in U.S. housing prices is nothing more than a combination of months of relentless propaganda proclaiming a “bottom” in this market – along with the minor boost to the economy from the Obama stimulus package, and the normal “seasonal strength” of this market in the summer.

Almost certainly these prices will resume their downward march in the next few weeks. The only thing which could alter this picture is if U.S. inflation (which the government pretends doesn't exist) should accelerate so rapidly that “up” becomes “down”. In other words, if U.S. inflation (currently around 7% in the real world) should heat-up to double-digits, we could see small nominal gains in U.S. prices – which in real dollars would still be steadily depreciating.

Meanwhile, in the commercial sector, the vacancy rate just hit its highest level in 5 years (reflecting the fact that this market hasn't been collapsing for as long as the housing market). It is a certainty that this rate will continue soaring higher – given that both corporate revenues and corporate earnings are still plunging downward at double-digit rates (see “Crash warnings abound for U.S. markets”).

This means that U.S. banks can expect sky-rocketing losses on their commercial mortgage portfolio (in this $6 trillion market). As I have pointed out in previous commentaries, U.S. banks have virtually nothing set aside for these losses. This was echoed by a presentation from the Federal Reserve to banking regulators last month – and is an “instant replay” of what happened with U.S. banks when the housing market crashed.

The main difference between this new source of mounting losses on this category of bank loans is that unlike with the crash in residential real estate, this crash comes at the same time that all other categories of U.S. debt are already at or near record-levels of delinquencies (i.e. loans where the banks are not getting paid). The combination of huge losses these banks must absorb on commercial defaults while they are not receiving payments from record numbers of borrowers in all other categories of debt, and having virtually no reserves to cover these losses creates a very painful dilemma for the banksters.

As I have stated unequivocally on numerous occasions (and which George Soros just echoed in a recent interview), U.S. big-banks remain insolvent. With new, rising losses and tiny capital cushions, it appears that some or all of them will be forced to get in line for their next series of government blank-cheques. The problem is how can the Wall Street crime syndicate beg for more hand-outs from the government while these fraud-factories claim to be making “profits”?

Once again, the perfect “recipe” for Wall Street appears to be to induce a broad, general panic – which could frighten both the spineless politicians and the American public enough for them to capitulate to more bankster blackmail. Given that most recent, U.S. economic data has still been terrible (despite what media spin-doctors would like us to believe), it would take nothing more than telling the truth to “pop” the U.S. equities bubble – and begin another fear cycle.

As a reminder, John Williams' “Shadowstats.com” (the most widely-accepted source for real numbers on the U.S. economy) has calculated current U.S. unemployment at over 20% (and still rising rapidly). Meanwhile, the fantasy-world presented by the propaganda-machine continues to pretend that things are getting better for the unemployed, and soon-to-be-unemployed.

This disconnect cannot continue. The absolute end-point for the fantasy-rally in U.S. equity markets is early December – the time at which it will be clear that this year's holiday shopping season will be a big disappointment for this consumer economy. However, there are an endless number of possible triggers between now and then (including the banksters proclaiming they need more hand-outs). For those who have continued to ignore six solid months of rising insider-selling, it's time to take your money and run.

Elizabeth Warren Highlights Washington's Losing Housing Battle

Elizabeth Warren Highlights Washington's Losing Housing Battle

by: Larry Doyle

October 11, 2009

Who in Washington will give you a straight answer? Elizabeth Warren.

Who is Elizabeth Warren?

Her Wikipedia bio reads:

Elizabeth Warren (born 1949) is the Leo Gottlieb Professor of Law at Harvard Law School, where she teaches contract law, bankruptcy, and commercial law. In the wake of the 2008-9 financial crisis, she has also become the chair of the Congressional Oversight Panel created to oversee the U.S. banking bailout, formally known as the Troubled Assets Relief Program. In 2007, she first developed the idea to create a new Consumer Financial Protection Agency, which President Barack Obama, Christopher Dodd, and Barney Frank are now advocating as part of their financial regulatory reform proposals.

In May 2009, Warren was named one of Time Magazine’s 100 Most InfluentialPeople in the World.

Ms. Warren consistently takes no prisoners or provides no pandering in making honest assessments of the interaction between Washington and Wall Street. She has called the banks on the carpet. She has called Secretary Geithner on the carpet. She has called Congress on the carpet. Why? A general lack of honesty, integrity, and transparency in dealing with the American public.

When she speaks, I listen.

What did she have to say Friday morning? In commenting on a recently released report on the effectiveness of government programs to support housing, Warren questioned the scalability and the permanence of the impact of the TARP funding. Bloomberg provides further color in writing Friday morning TARP Oversight Group Says Treasury Mortgage Plan Not Effective.

The report highlights,

“Rising unemployment, generally flat or even falling home prices and impending mortgage-rate resets threaten to cast millions more out of their homes,” the report said. “The panel urges Treasury to reconsider the scope, scalability and permanence of the programs designed to minimize the economic impact of foreclosures and consider whether new programs or program enhancements could be adopted.”

New programs or program enhancements? On Thursday I opined in Washington Needs a New Housing Model:

While the administration swims upstream on this issue, bank policy of tight credit and restrictive lending only further exacerbates the housing market. Make no mistake, though, banks are taking that approach to tight credit at the behest of regulators who know the level of losses in the banking system and are trying to preserve the industry as a whole.

I like a rallying equity market as much as anybody, but I wouldn’t spend any paper gains just yet. Why? The new housing model is displaying that:

“As defaults become more common, the social stigma attached with defaulting will likely be reduced, especially if there continues to be few repercussions for people who walk away from their loans,” concluded Sapienza. “This has an adverse effect on homeowners who do pay their mortgages, and the after-effects of more defaults and more price collapse could be economic catastrophe.”

This model needs some quick-dry crazy glue, which could only be applied in the form of a serious principal reduction program. Banks would take immediate and massive hits to capital which they clearly won’t accept.

So how can we generate some support for housing?

Aside from a principal reduction program, the penalty for those who would strategically default on their mortgage needs to be far more onerous.

The principal reduction would negatively impact bank earnings. Too bad. The banks are feeding at the taxpayer trough currently and would not be here without the bailouts. The individuals who are capable of making their payments need to accept the moral responsibility that is embedded in a contract.

Although given the massive violation of moral hazards and breaking of contracts by Uncle Sam, that old man does not have a lot of credibility on that front.

What do we really learn here? Ultimately the market is the market and efforts to manipulate or support a falling market will only be temporary. The market needs to find the clearing level where private money will purchase properties. That private money will wait while Uncle Sam continues to try to prop the market.

In the meantime, do not expect any meaningful support for housing.

by: Larry Doyle

October 11, 2009

Who in Washington will give you a straight answer? Elizabeth Warren.

Who is Elizabeth Warren?

Her Wikipedia bio reads:

Elizabeth Warren (born 1949) is the Leo Gottlieb Professor of Law at Harvard Law School, where she teaches contract law, bankruptcy, and commercial law. In the wake of the 2008-9 financial crisis, she has also become the chair of the Congressional Oversight Panel created to oversee the U.S. banking bailout, formally known as the Troubled Assets Relief Program. In 2007, she first developed the idea to create a new Consumer Financial Protection Agency, which President Barack Obama, Christopher Dodd, and Barney Frank are now advocating as part of their financial regulatory reform proposals.

In May 2009, Warren was named one of Time Magazine’s 100 Most InfluentialPeople in the World.

Ms. Warren consistently takes no prisoners or provides no pandering in making honest assessments of the interaction between Washington and Wall Street. She has called the banks on the carpet. She has called Secretary Geithner on the carpet. She has called Congress on the carpet. Why? A general lack of honesty, integrity, and transparency in dealing with the American public.

When she speaks, I listen.

What did she have to say Friday morning? In commenting on a recently released report on the effectiveness of government programs to support housing, Warren questioned the scalability and the permanence of the impact of the TARP funding. Bloomberg provides further color in writing Friday morning TARP Oversight Group Says Treasury Mortgage Plan Not Effective.

The report highlights,

“Rising unemployment, generally flat or even falling home prices and impending mortgage-rate resets threaten to cast millions more out of their homes,” the report said. “The panel urges Treasury to reconsider the scope, scalability and permanence of the programs designed to minimize the economic impact of foreclosures and consider whether new programs or program enhancements could be adopted.”

New programs or program enhancements? On Thursday I opined in Washington Needs a New Housing Model:

While the administration swims upstream on this issue, bank policy of tight credit and restrictive lending only further exacerbates the housing market. Make no mistake, though, banks are taking that approach to tight credit at the behest of regulators who know the level of losses in the banking system and are trying to preserve the industry as a whole.

I like a rallying equity market as much as anybody, but I wouldn’t spend any paper gains just yet. Why? The new housing model is displaying that:

“As defaults become more common, the social stigma attached with defaulting will likely be reduced, especially if there continues to be few repercussions for people who walk away from their loans,” concluded Sapienza. “This has an adverse effect on homeowners who do pay their mortgages, and the after-effects of more defaults and more price collapse could be economic catastrophe.”

This model needs some quick-dry crazy glue, which could only be applied in the form of a serious principal reduction program. Banks would take immediate and massive hits to capital which they clearly won’t accept.

So how can we generate some support for housing?

Aside from a principal reduction program, the penalty for those who would strategically default on their mortgage needs to be far more onerous.

The principal reduction would negatively impact bank earnings. Too bad. The banks are feeding at the taxpayer trough currently and would not be here without the bailouts. The individuals who are capable of making their payments need to accept the moral responsibility that is embedded in a contract.

Although given the massive violation of moral hazards and breaking of contracts by Uncle Sam, that old man does not have a lot of credibility on that front.

What do we really learn here? Ultimately the market is the market and efforts to manipulate or support a falling market will only be temporary. The market needs to find the clearing level where private money will purchase properties. That private money will wait while Uncle Sam continues to try to prop the market.

In the meantime, do not expect any meaningful support for housing.

Friday, October 9, 2009

FCC Blog Advertising Disclosure

Disclosure

We at "Hoboken RE.ality" would like to take this opportunity to notify our thousands of interested readers that we are way ahead of the curve on this one! Since transparency on the RE market has been our foremost mandate, it goes without saying that we receive no compensation in any form, from any parties whatsoever; especially RE developers, brokers and investors!

We at "Hoboken RE.ality" would like to take this opportunity to notify our thousands of interested readers that we are way ahead of the curve on this one! Since transparency on the RE market has been our foremost mandate, it goes without saying that we receive no compensation in any form, from any parties whatsoever; especially RE developers, brokers and investors!

Wednesday, October 7, 2009

Higher interest rates and the end of the tax credit imply lower future house prices.

Mortgage Applications Surge as Homebuyers Seek to Benefit from Tax Credit

Higher interest rates and the end of the tax credit imply lower future house prices.

DEAN BAKER, CEPR

The Mortgage Bankers Association (MBA) reported that its purchase mortgage applications index jumped 13.2 percent last week to its highest level since February. This is likely attributable to a last ditch effort by homebuyers to close on a house before the $8,000 first-time homebuyers tax credit is scheduled to expire at the end of November. Given the lead-time between contracting and closing (the credit depends on the date of closing), we are approaching the end of the period in which a contract can be expected to close in time to qualify for the credit.

Low interest rates were also a factor pushing demand last week. The interest rate on 30-year mortgages averaged 4.89 percent according to the MBA. This is the third consecutive week that it was below 5 percent. The low mortgage rates also led to a surge in applications for refinancing. This index was up 18.2 percent from the prior week.

With Congress debating a renewal of the first-time buyers credit, it is worth noting its likely impact on the market. According to several estimates, it will lead to close to 350,000 additional home purchases by the time it expires. It presumably also had a substantial impact on stabilizing house prices.

According the National Association of Realtors, 40 percent of buyers are now first-time buyers, most of whom are eligible for the credit. In principle these people would be willing to pay $8,000 more for a home than they would have been willing to pay without the credit. This is 4.7 percent of the median house price for an existing home. If just half of the credit was reflected in higher house prices, it would mean that the median house price is 2.4 percent higher than it would be in the absence of the credit. This, alone, would go far toward stabilizing house prices. Of course the extraordinarily low interest rates available at present are also a factor lifting house prices.

This raises the issue of what happens to house prices when interest rates return to normal and the credit eventually expires (even if the credit is extended beyond November, presumably Congress will not always support taxing the general population to give people $8,000 to buy a home). It is likely at that point that house prices will decline further, presumably completing the deflation of the bubble. This could mean that many of the people who buy homes in the current market are likely to sell them at a substantial loss (after adjusting for inflation). Temporarily propping up house prices, so that a new set of homebuyers can incur losses, is a policy of questionable merit.

The extension of the tax credit is likely to have limited impact in boosting sales in the future largely because it has been relatively successful in pulling demand forward. Most of the people who bought homes because of the credit would have otherwise bought homes in 2010 or even 2011. Because they bought a home this year, they will not be in the market in future years. Therefore, the pool of potential first-time homebuyers is much lower today than it was last February.

Whether or not the credit is extended, the outlook for the market in the near future is almost certain to darken. The number of mortgage delinquencies continues to rise. With the economy continuing to lose jobs and many homeowners having exhausted their savings and their unemployment benefits, there will certainly be more distressed sales in the future. In addition, it seems unlikely that interest rates will remain at the extraordinarily low levels that they have been at in recent months. We are approaching the end of the period in which the Fed has committed to buy mortgage-backed securities, so unless they extend their purchases, mortgage rates will almost certainly be rising in the next few months. In short, there are many factors suggesting that the housing market will weaken with more supply and weakened demand. There is really nothing pointing in the opposite direction.

-- October 7, 2009

Higher interest rates and the end of the tax credit imply lower future house prices.

DEAN BAKER, CEPR

The Mortgage Bankers Association (MBA) reported that its purchase mortgage applications index jumped 13.2 percent last week to its highest level since February. This is likely attributable to a last ditch effort by homebuyers to close on a house before the $8,000 first-time homebuyers tax credit is scheduled to expire at the end of November. Given the lead-time between contracting and closing (the credit depends on the date of closing), we are approaching the end of the period in which a contract can be expected to close in time to qualify for the credit.

Low interest rates were also a factor pushing demand last week. The interest rate on 30-year mortgages averaged 4.89 percent according to the MBA. This is the third consecutive week that it was below 5 percent. The low mortgage rates also led to a surge in applications for refinancing. This index was up 18.2 percent from the prior week.

With Congress debating a renewal of the first-time buyers credit, it is worth noting its likely impact on the market. According to several estimates, it will lead to close to 350,000 additional home purchases by the time it expires. It presumably also had a substantial impact on stabilizing house prices.

According the National Association of Realtors, 40 percent of buyers are now first-time buyers, most of whom are eligible for the credit. In principle these people would be willing to pay $8,000 more for a home than they would have been willing to pay without the credit. This is 4.7 percent of the median house price for an existing home. If just half of the credit was reflected in higher house prices, it would mean that the median house price is 2.4 percent higher than it would be in the absence of the credit. This, alone, would go far toward stabilizing house prices. Of course the extraordinarily low interest rates available at present are also a factor lifting house prices.

This raises the issue of what happens to house prices when interest rates return to normal and the credit eventually expires (even if the credit is extended beyond November, presumably Congress will not always support taxing the general population to give people $8,000 to buy a home). It is likely at that point that house prices will decline further, presumably completing the deflation of the bubble. This could mean that many of the people who buy homes in the current market are likely to sell them at a substantial loss (after adjusting for inflation). Temporarily propping up house prices, so that a new set of homebuyers can incur losses, is a policy of questionable merit.

The extension of the tax credit is likely to have limited impact in boosting sales in the future largely because it has been relatively successful in pulling demand forward. Most of the people who bought homes because of the credit would have otherwise bought homes in 2010 or even 2011. Because they bought a home this year, they will not be in the market in future years. Therefore, the pool of potential first-time homebuyers is much lower today than it was last February.

Whether or not the credit is extended, the outlook for the market in the near future is almost certain to darken. The number of mortgage delinquencies continues to rise. With the economy continuing to lose jobs and many homeowners having exhausted their savings and their unemployment benefits, there will certainly be more distressed sales in the future. In addition, it seems unlikely that interest rates will remain at the extraordinarily low levels that they have been at in recent months. We are approaching the end of the period in which the Fed has committed to buy mortgage-backed securities, so unless they extend their purchases, mortgage rates will almost certainly be rising in the next few months. In short, there are many factors suggesting that the housing market will weaken with more supply and weakened demand. There is really nothing pointing in the opposite direction.

-- October 7, 2009

Subscribe to:

Posts (Atom)